Table of Content

A construction loan is a short-term loan that covers only the costs of custom home building. This is different from a mortgage, and it’s considered specialty financing. Once the home is built, the prospective occupant must apply for a mortgage to pay for the completed home.

The home’s location and amenities matter, and you don’t feel like lowering your standards or settling. It is actually common to stumble across a few builders who do not require a specific type of financing to build from the ground up. Construction loans are available to anyone who meets the qualifying eligibility requirements. Granite's inspectors act as the eyes and ears of the project, verifying all construction work is in place as per the plans and specifications prior to the release of funds. Our new online mortgage application makes buying and refinancing even easier.

What's the Difference between a Home Construction Loan and a Mortgage?

That said, not everyone has the home equity to secure a loan the size they need for major construction, so each of these three options can offer benefits for different kinds of borrowers. If you don’t own a home yet or haven’t built up substantial equity in one, a HELOC isn’t likely to be an option for your building project. Despite higher interest charges, a 30-year loan is the most popular because it offers the lowest monthly mortgage payment. If approved, the borrower starts drawing funds in conjunction with each phase of the project, typically only repaying interest during construction. Throughout construction, an appraiser or inspector assesses the build to authorize more funds. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens.

You do not have to pay the builder up front and tie up a large amount of capital. All the while praying you are able to finance the home post build. Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear.

Home Loans and Mortgages | New Prague, MN

During this time, the property must be built and a certificate of occupancy should be issued. Qualifying for a construction mortgage involves not only meeting the lender’s borrower standards, but getting your builder approved. Construction mortgages allow you to pay for the cost of custom building a new home.

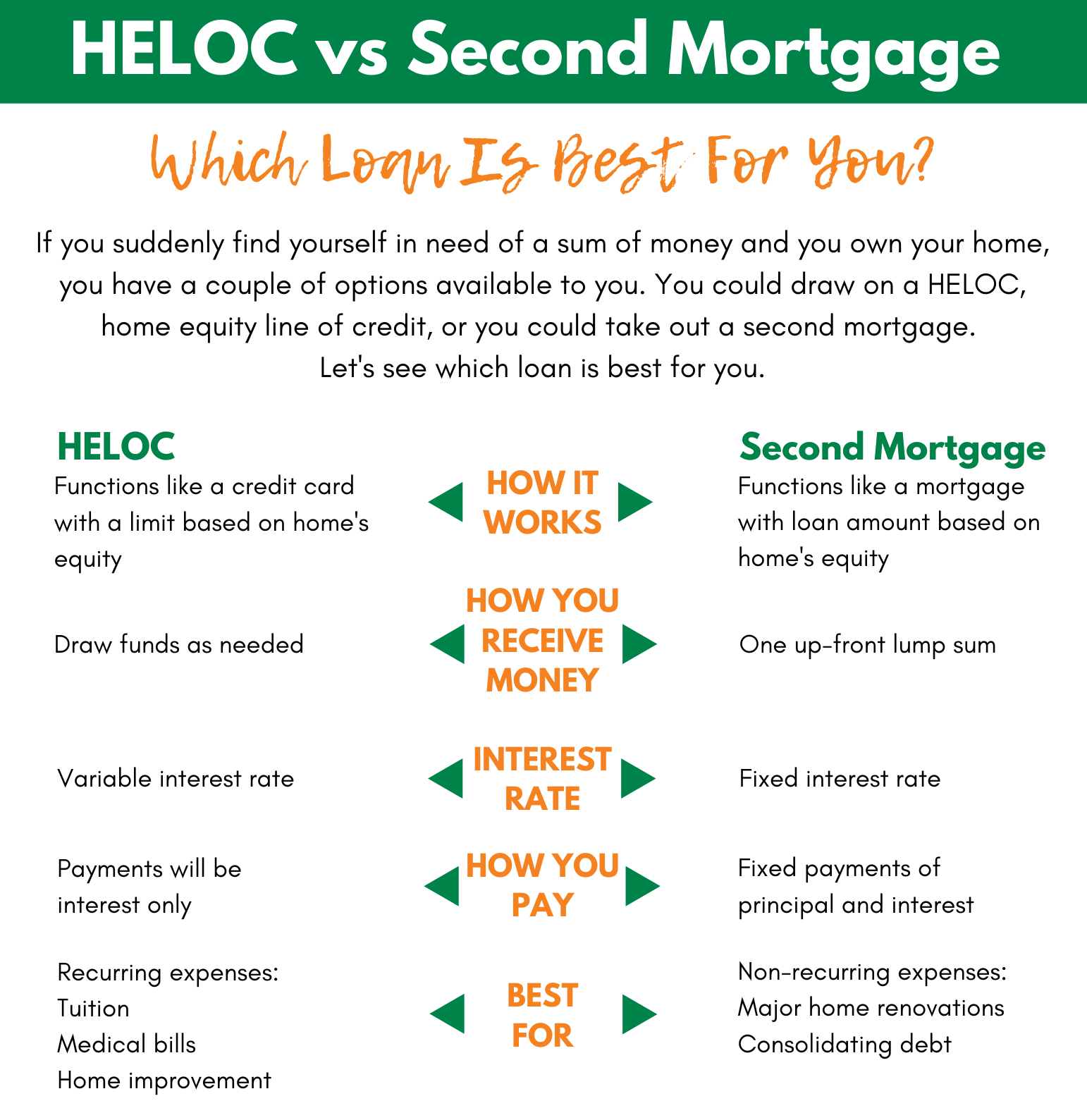

Whether you get a HELOC, an equity loan or a cash back refinance, you will pay the loan over many years, which will reduce your monthly payments. However, you will need to pay much more in interest than a construction or home improvement loan. Check the current HELOC rates and home equity loan credit from national finance companies. If you’re an active-duty service member or veteran, you may even qualify for a VA construction loan from the Department of Veterans Affairs .

Home Financing Options

They’re distinctly different from mortgages, but those differences can be confusing. Get the latest mortgage rates for purchase or refinance from reputable lenders at realtor.com®. Simply enter your home location, property value and loan amount to compare the best rates. For a more advanced search, you can filter your results by loan type for 30 Year Fixed, 15 Year Fixed and 5 Year ARM Prague mortgages.

Construction loans from Johnson Bank help you finance your new home from the ground up. We can provide the financing you need to get your project off the ground, whether you’re a first-time homebuilder or an experienced developer. Our construction loans come with competitive rates and terms, and we can work with you to tailor a loan that meets your needs. Contact us today to learn more about our construction loan options. As mentioned, construction loans are short-term loans, usually no longer than a year in length.

LOAN REQUIREMENTS

There is no definitive answer to this question as it depends on a variety of factors including your personal financial situation. Some people may find that a 30-year mortgage is a smart choice because it allows them to keep their monthly payments low. Others may find that a shorter-term mortgage is a better option because it saves them money in interest over the life of the loan. Ultimately, it is important to weigh all of your options and make the decision that is best for your unique circumstances. Seniors should consider applying for a mortgage for a variety of reasons later in life.

If a homeowner stays in the property for the duration of the loan and makes his or her payments as agreed, they will be able to pay off the mortgage in 40 years. It is not a “qualified mortgage” according to the Consumer Financial Protection Bureau. Monthly payments are typically lower than those of shorter-term loans. You will end up paying more in interest as you make more payments over time.

Note that the requirements for getting approved don’t end at financial records. You also need to show your lender a comprehensive list of construction details, a.k.a. “blue book”. You should also prove that a qualified builder will take on the project.

Once the building is completed, the borrower usually gets the loan converted into a mortgage, and both loans get rolled into one. When you take out a mortgage, your lender makes a lump sum payment to the seller of the house. With a construction loan, your lender disburses the money in increments as your builder completes different phases of your new home.

With construction loans, you will typically be expected to make only interest payments during the construction stage. Additionally, borrowers are typically only obligated to repay interest on any funds drawn to date until construction is completed. Construction-to-permanent, which starts out as a construction loan and converts to a regular mortgage upon building completion, requires only one closing. Construction loan is a short-term loan that a builder or home buyer takes out to construct a new home or building. This type of financing can also be used by borrowers looking to finance restoration or historic preservation projects.

A construction mortgage works a bit differently than a regular home loan. For starters, they are shorter term, and typically have higher interest rates than traditional long-term mortgages. A construction mortgage is most commonly used by someone who wants a new-construction home and needs funds to pay the builders as they complete each phase of construction. Or it could be used to hire a contractor to construct a new home on property or renovate an existing home. Whether its a construction loan, a renovation loan, a HELOC or any other number of options, finding the right way to borrow money for your next home doesnt have to be too hard. Both of these home construction loan products can work for your house improvement needs.

Finding a property that suits all your needs is not an easy feat. While building your dream home is a big project, it gives you flexibility and freedom to construct something perfect for you, from paint to pavers and everything in between. One good aspect of an end loan is that the mortgage application for a newly constructed home is the same as it is for any other home. Less complicated is always appreciated when it comes to financing applications.

No comments:

Post a Comment